Crude posts another weekly decline as surplus outlook outweighs geopolitical support

Crude suffered a second consecutive weekly loss as easing disruption fears weighed against increasing signals of structural oversupply. Diplomatic engagement between the US and Iran reduced the immediacy of escalation risk, yet unresolved tensions preserved a residual geopolitical premium.

The latest Oil Market Report from the IEA indicates global inventories are expanding at the fastest pace since the pandemic, with stockpiles rising sharply and OECD inventories returning above historical norms. Demand growth expectations have been revised lower and the agency now anticipates a surplus exceeding 3.7 MMBbl/d in 2026, underscoring the scale of the emerging imbalance.

The EIA’s February Short-Term Energy Outlook reinforces this direction. Global inventories are projected to build materially in 2026 and remain elevated into 2027 as supply growth continues to outpace demand. WTI spot prices are expected to average near $53/Bbl in 2026 and decline further in 2027, although OPEC+ restraint and continued Chinese strategic stockpiling may slow the pace of downside.

Not all market participants share the same interpretation of emerging oversupply. Goldman Sachs’ Dean Struyven notes that excess barrels are concentrated in regions with limited influence on benchmark pricing, while several OPEC+ members are signaling room to restart supply increases as early as April, arguing fears of a broad global glut may be overstated. The alliance’s final production decision may ultimately hinge on the trajectory of US policy toward Iran and whether geopolitical tensions escalate or continue to ease.

Taken together, the week’s developments reinforce a market shifting its focus back toward fundamentals rather than geopolitics. While unresolved Middle East risk can still generate episodic volatility, expanding inventories and slowing demand growth continue to define the medium-term outlook. AEGIS maintains a bearish view, and unless disruption risk materially removes supply, rallies are likely to fade as crude re-anchors to expectations of a structurally looser global balance.

Crude Oil Factors

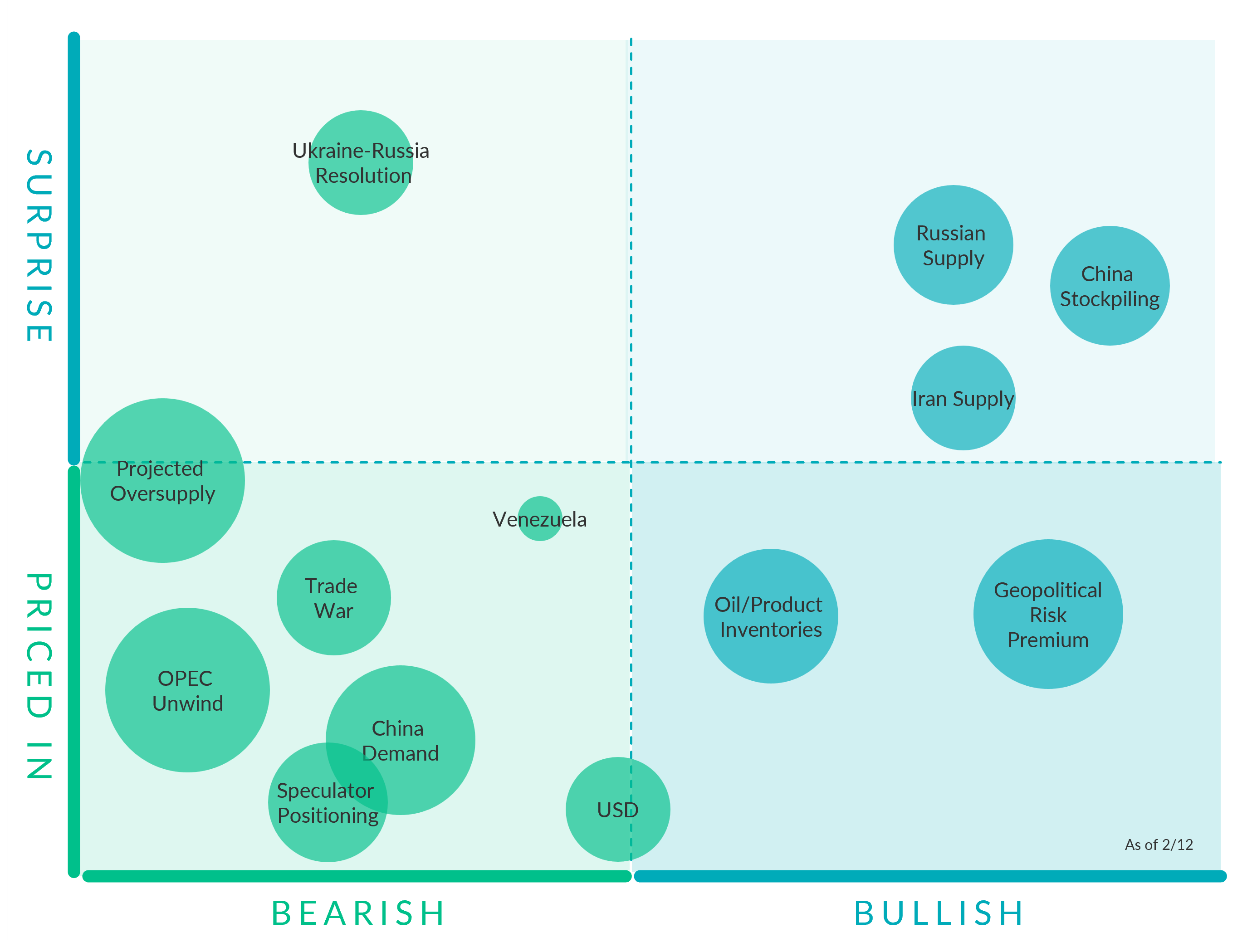

Geopolitical Risk Premium. (Bullish, Slightly Priced In) The risk premium has faded this week as President Trump said he informed Israeli Prime Minister Benjamin Netanyahu that Washington intends to continue diplomatic engagement with Iran, emphasizing a preference for a negotiated agreement.

Speculator Positioning (Bearish, Priced In) Bullish call options have traded at a premium to puts for the longest stretch in roughly 14 months, while hedge funds have lifted net-bullish positions to the highest level since August. This suggests speculative positioning is skewed toward upside tail risk tied to Iran, even as underlying fundamentals remain less supportive.

Oil/Product Inventories. (Bullish, Priced In) The latest Oil Market Report from the IEA indicates global inventories are expanding at the fastest pace since the pandemic, with stockpiles rising sharply and OECD inventories returning above historical norms. Demand growth expectations have been revised lower and the agency now anticipates a surplus exceeding 3.7 MMBbl/d in 2026, underscoring the scale of the emerging imbalance.

OPEC+ Quotas. (Bullish, Priced In) OPEC+ has paused planned oil production increases through Q1 2026, keeping output targets unchanged for January–March after raising quotas by about 2.9 m b/d through late 2025. Eight key producers, including Saudi Arabia and Russia, reaffirmed the freeze at their early January meeting, emphasizing market stability amid a looming surplus and seasonal demand patterns.

OPEC Unwind. (Bearish, Mostly Priced in) Several OPEC+ members are signaling room to restart supply increases as early as April, arguing fears of a broad global glut may be overstated. The alliance’s final production decision may ultimately hinge on the trajectory of US policy toward Iran and whether geopolitical tensions escalate or continue to ease.

China Stockpiling. (Bullish, Surprise)A significant portion of recent global stock builds has been absorbed into Chinese strategic reserves, effectively converting what would otherwise appear as excess supply into incremental demand. The EIA expects this pattern to persist through 2026, with China continuing to add crude to storage at a pace near 1 MMBbl/d before moderating in 2027. This behavior helps cushion near-term price declines by tightening observable market balances, even as underlying global supply growth continues to exceed consumption. Once strategic stockpiling slows, however, the buffering effect diminishes, leaving prices more directly exposed to the broader surplus implied by rising non-OPEC production and moderating demand growth.

USD (Bearish, Priced In) The dollar has acted as a secondary tailwind for crude, with recent DXY weakness linked to easing rate expectations. Historically, a softer dollar has coincided with stronger commodity prices, reinforcing oil’s recent gains without altering the underlying supply-demand balance.

Ukraine-Russia Resolution. (Bearish, Surprise) Ukrainian President Volodymyr Zelensky said he agreed to work on a peace plan drafted by the US and Russia aimed at ending the war in Ukraine. A peace deal, if followed by the elimination of sanctions on Russian oil over its invasion of Ukraine, could unleash supply from the world's third largest producer.

Trade War. (Bearish, Mostly Priced In) There has been an increase in tit-for-tat trade tension between the US and China, with China sanctioning the US unit of Hanwha Ocean Co., a South Korean shipping major, and warned of additional retaliatory actions against the industry. However, President Trump said high tariffs on China were “not viable,” suggesting potential for de-escalation even as broader tensions remain elevated.

Projected Oversupply. (Bearish, Mostly Surprise) The latest EIA STEO reinforces that these geopolitical episodes are occurring against a backdrop of persistent oversupply. The STEO forecasts global oil inventories will continue to build through 2026, with implied stock builds averaging roughly 2.8 MMBbl/d, as global production growth outpaces demand.

Iran Supply. (Bullish, Slight Surprise) Iran continues to supply roughly 3.2–3.3 mb/d, with exports near multi-year highs around 1.7–2.0 mb/d. With flows still intact, Iran’s impact on crude has been more about potential disruption than realized supply losses.

Russian Supply. (Bullish, Slight Surprise) Russian exports also faced growing logistical friction as US sanctions pushed more barrels into shadow-fleet channels. Strikes on refineries and export facilities have slowed transit and increased reliance on intermediaries, lifting Russian oil-on-water above 180 MMBbl.

Venezuela. (Bearish, Slight Priced In) Venezuela remains a constrained but potentially growing source of supply, producing roughly ~0.8–1.1 mb/d in recent months, far below historical capacity and less than 1% of global output.

Recent policy shifts and easing restrictions could allow incremental increases, with analysts suggesting output could rise by roughly 30% from current levels in the short to medium term, though structural limitations and infrastructure decay cap near-term upside.

Commodity Interest Trading involves risk and, therefore, is not appropriate for all persons; failure to manage commercial risk by engaging in some form of hedging also involves risk. Past performance is not necessarily indicative of future results. There is no guarantee that hedge program objectives will be achieved. Certain information contained in this research may constitute forward-looking terminology, such as “edge,” “advantage,” ‘opportunity,” “believe,” or other variations thereon or comparable terminology. Such statements and opinions are not guarantees of future performance or activities. Neither this trading advisor nor any of its trading principals offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program.