Hormuz shipping crisis drives crude higher as Gulf storage constraints loom

Crude markets surged this week as the conflict between the US, Israel and Iran escalated into a broader regional disruption that threatened flows through the Strait of Hormuz. The WTI prompt month contract ultimately settled at $90.90/Bbl, a $23.88 increase from last week’s $67.02/Bbl close as markets rapidly priced a geopolitical risk premium into crude. Shipping activity through the waterway slowed dramatically as insurers and operators suspended transits, forcing vessels to anchor outside the strait and disrupting one of the most important arteries in global energy trade. Roughly one fifth of global oil supply normally moves through the corridor, making even temporary interruptions highly consequential for prompt balances.

The rally also triggered a wave of producer hedging as companies moved to lock in improved price levels. As an oil and gas hedging advisor, we recorded a record volume of crude hedged on Monday March 2, with activity on March 3 also exceptionally heavy and just shy of Monday’s record. The surge in hedging reflects producers taking advantage of the rapid repricing in crude while geopolitical uncertainty remains elevated.

The market’s primary concern is no longer simply the possibility of conflict but the logistical bottlenecks emerging across Gulf producers. With tanker access severely restricted, exports from the region have become increasingly constrained, forcing some producers to begin curtailing output as storage facilities approach capacity. Gulf storage sites are filling rapidly while several regional exporters have explored rerouting barrels through alternative pipelines and ports where available. While countries such as Saudi Arabia and the UAE can redirect some flows through pipelines toward the Red Sea or Fujairah, the available bypass capacity is limited and cannot fully replace seaborne exports through the strait.

Storage constraints represent the next major risk if disruptions persist. JP Morgan estimates Gulf producers collectively hold just under 400MMBbls of total available storage, equivalent to roughly 25 days of normal production before tanks fill and output shut ins become unavoidable. Early signs of this pressure are already emerging. Iraq has begun shutting in roughly 1.5 MMBbl/d of production as tanks fill, with the potential for losses to expand toward 3 MMBbl/d if export constraints persist. The Wall Street Journal also reported that Kuwait has started curbing production at some fields as storage capacity tightens.

For now the trajectory of crude will hinge on one variable above all others. If tanker traffic through the Strait of Hormuz normalizes quickly the geopolitical premium embedded in prices could fade just as rapidly. If shipping disruptions persist long enough for storage limits to bind across Gulf producers the market could transition from a risk premium story into a confirmed supply loss scenario.

Crude Oil Factors

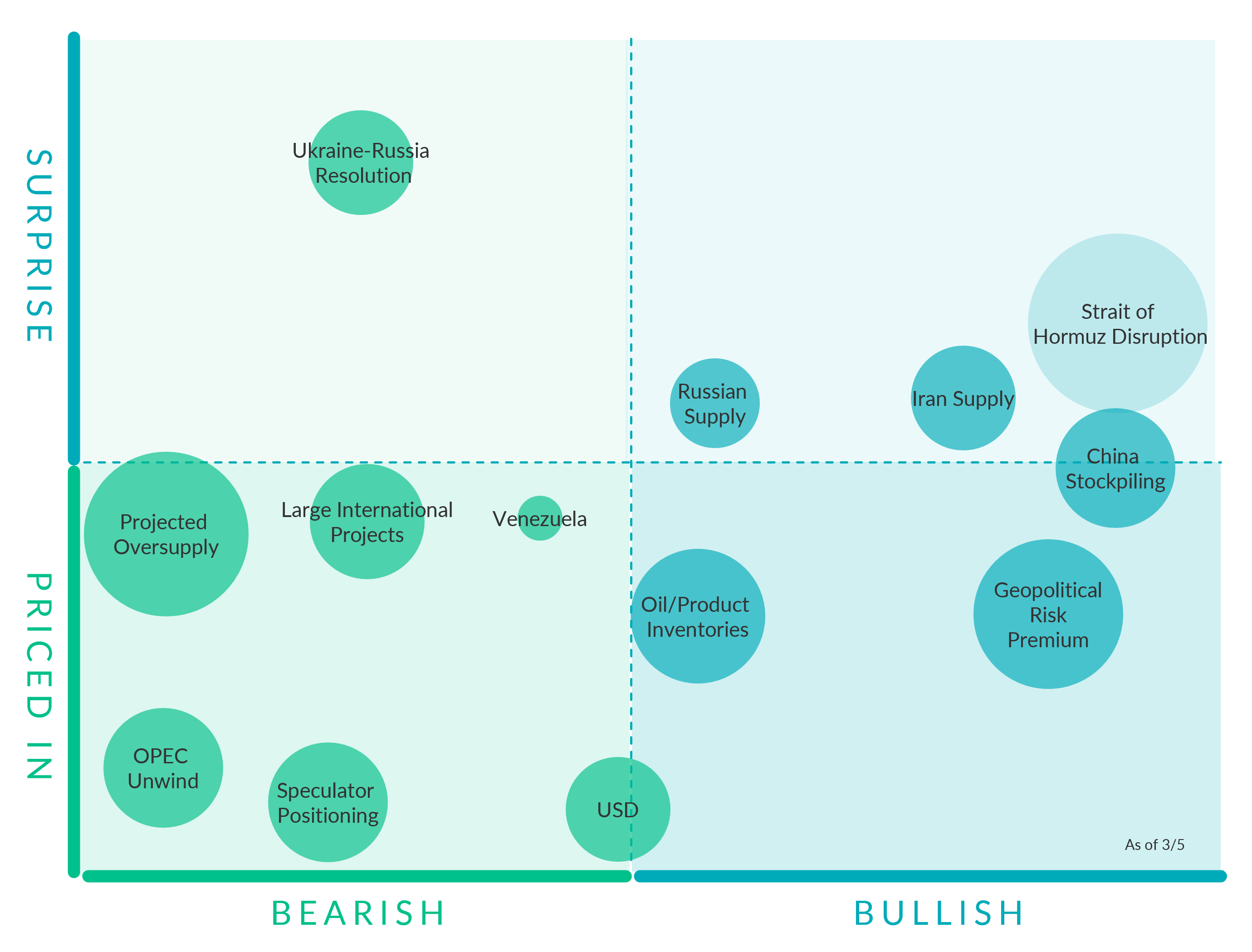

Geopolitical Risk Premium. (Bullish, Slightly Priced In) Crude futures rallied into the weekend as markets braced for potential escalation surrounding upcoming nuclear negotiations. Iranian Foreign Minister Abbas Araqchi said technical teams would meet in Vienna starting Monday and that political talks will resume next week. However, concerns about a potential US strike on Iran is supporting crude prices, with the US military buildup in the region now the largest since the 2003 Iraq invasion, reinforcing a geopolitical risk premium.

Speculator Positioning (Bearish, Priced In) Elevated geopolitical risk is increasingly reflected in oil market positioning. According to Bloomberg, upside-focused options have traded at sustained premiums to downside protection for much of the year.

Oil/Product Inventories. (Bullish, Priced In) The latest Oil Market Report from the IEA indicates global inventories are expanding at the fastest pace since the pandemic, with stockpiles rising sharply and OECD inventories returning above historical norms. Demand growth expectations have been revised lower and the agency now anticipates a surplus exceeding 3.7 MMBbl/d in 2026, underscoring the scale of the emerging imbalance.

OPEC Unwind. (Bearish, Mostly Priced in) Several OPEC+ delegates indicated the group is likely to move forward with a gradual return of curtailed barrels when it convenes this weekend to assess April production policy. Discussions have centered on a potential 137 MBbl/d increase, consistent with the incremental adjustments implemented late last year.

China Stockpiling. (Bullish, Surprise) A significant portion of recent global stock builds has been absorbed into Chinese strategic reserves, effectively converting what would otherwise appear as excess supply into incremental demand. The EIA expects this pattern to persist through 2026, with China continuing to add crude to storage at a pace near 1 MMBbl/d before moderating in 2027. This behavior helps cushion near-term price declines by tightening observable market balances, even as underlying global supply growth continues to exceed consumption. Once strategic stockpiling slows, however, the buffering effect diminishes, leaving prices more directly exposed to the broader surplus implied by rising non-OPEC production and moderating demand growth.

USD (Bearish, Priced In) The recent U.S. Supreme Court decision overturning former President Trump’s broad tariff authority led to a modest dip in the U.S. dollar as investor uncertainty eased and Treasury yields rose, reflecting a short-term softening in safe-haven demand. In oil markets, a weaker dollar can be slightly supportive for crude prices by making oil cheaper in foreign currency terms, but the ongoing geopolitical risk premium from Middle East tensions continues to be the dominant driver of crude strength at the moment.

Large International Projects (Bearish, Priced In) Major offshore developments in countries like Brazil and Guyana are now translating years of capital-intensive investment and long development timelines into meaningful production growth. These deepwater projects are finally ramping volumes into the global market, adding steady, non-OPEC supply that contributes to medium-term balance loosening and moderates structural upside pressure on crude prices.

Ukraine-Russia Resolution. (Bearish, Surprise) Talks between Russia and the Ukraine are ongoing and being mediated by the US, but no tangible results are yet to arise that would bring an end to the war in Ukraine. A peace deal, if followed by the elimination of sanctions on Russian oil over its invasion of Ukraine, could unleash supply from the world's third largest producer.

Trade War. (Bearish, Mostly Priced In)The US Supreme Court ruled 6–3 that former President Trump’s broad global tariffs imposed under emergency powers were unconstitutional, dealing a significant setback to his trade agenda. However, efforts to maintain or reimplement tariffs under alternative legal authorities have preserved uncertainty around US trade policy, keeping the risk of renewed trade tensions and demand headwinds in play for global markets.

Projected Oversupply. (Bearish, Mostly Surprise) The latest EIA STEO reinforces that these geopolitical episodes are occurring against a backdrop of persistent oversupply. The STEO forecasts global oil inventories will continue to build through 2026, with implied stock builds averaging roughly 2.8 MMBbl/d, as global production growth outpaces demand.

Iran Supply. (Bullish, Slight Surprise) Iran continues to supply roughly 3.2–3.3 mb/d, with exports near multi-year highs around 1.7–2.0 mb/d. With flows still intact, Iran’s impact on crude has been more about potential disruption than realized supply losses.

Russian Supply. (Bullish, Slight Surprise) Russian exports also faced growing logistical friction as US sanctions pushed more barrels into shadow-fleet channels. Strikes on refineries and export facilities have slowed transit and increased reliance on intermediaries, lifting Russian oil-on-water above 180 MMBbl.

Venezuela. (Bearish, Slight Priced In) Venezuela remains a constrained but potentially growing source of supply, producing roughly ~0.8–1.1 mb/d in recent months, far below historical capacity and less than 1% of global output.

Recent policy shifts and easing restrictions could allow incremental increases, with analysts suggesting output could rise by roughly 30% from current levels in the short to medium term, though structural limitations and infrastructure decay cap near-term upside.

Strait of Hormuz Disruption (Bullish, Surprise) Shipping activity through the Strait of Hormuz remains severely constrained as insurers and operators continue suspending transits through the waterway amid ongoing hostilities between the US, Israel and Iran. With tanker traffic still limited, Gulf producers are increasingly facing export bottlenecks that could force additional production shut ins if the disruption persists.

Commodity Interest Trading involves risk and, therefore, is not appropriate for all persons; failure to manage commercial risk by engaging in some form of hedging also involves risk. Past performance is not necessarily indicative of future results. There is no guarantee that hedge program objectives will be achieved. Certain information contained in this research may constitute forward-looking terminology, such as “edge,” “advantage,” ‘opportunity,” “believe,” or other variations thereon or comparable terminology. Such statements and opinions are not guarantees of future performance or activities. Neither this trading advisor nor any of its trading principals offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program.